[ad_1]

Already deflated by overwhelmingly gentle climate up to now this winter, regional pure gasoline ahead costs noticed a mixture of typically small changes in the course of the Feb. 2-8 buying and selling interval, NGI’s Ahead Look information present.

Having descended into sub-$3 territory, benchmark Henry Hub conceded one other 6.9 cents for March mounted value buying and selling, ending the interval at $2.404/MMBtu. Quite a few Decrease 48 hubs completed inside a dime of unchanged week/week.

Within the Midwest, Chicago Citygate March mounted costs ended the interval at $2.498, up 0.3 cents. Within the Northeast, Transco Zone 6 NY shed 9.4 cents to fall to $2.974.

Moderation Out West

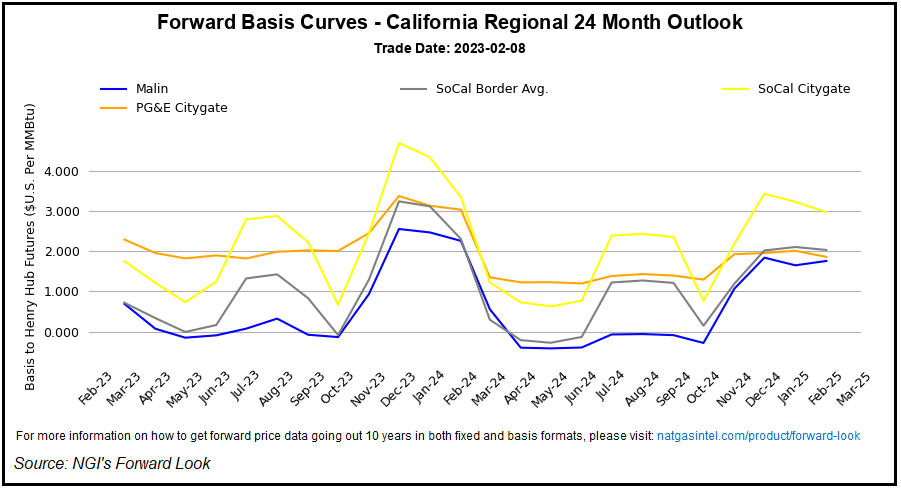

For some Western markets that noticed elevated costs within the week-earlier interval, reductions have been steeper. Northwest Sumas March mounted costs tumbled $1.349 to $3.141. Malin dropped 53.6 cents to finish at $3.089.

In California, SoCal Citygate dropped 75.1 cents to common $4.154 for March supply, whereas PG&E Citygate shed 49.5 cents to fall to $4.692.

As of Thursday, Redwood Path flows into PG&E had proven a “fast” decline of 298 MMcf/d for the reason that begin of the week, largely a results of declining receipts from Ruby at Malin “traced again to a sudden tightening in flows from Overthrust,” in accordance with Wooden Mackenzie analyst Quinn Schulz.

Stream information additionally confirmed a coinciding improve in volumes flowing from Overthrust onto Kern River heading towards Southern California, in accordance with the analyst.

Since Monday, “complete Kern deliveries onto SoCal at Wheeler Ridge and Kramer Junction additionally jumped by 145 MMcf/d,” Schulz mentioned. This, together with a drop in demand within the SoCal system, “helped loosen SoCal by a noticeable quantity throughout this time. For context, this helped SoCal cross right into a surplus of gasoline, with the ratio of pipeline receipts versus complete demand growing by almost 10%, from 92% to 101%.”

In the meantime, up to date climate modeling Thursday confirmed below-normal temperatures reserved for the western Decrease 48 within the 11- to 15-day time-frame, with unseasonably heat situations anticipated to blanket the japanese half of the nation, in accordance with Maxar’s Climate Desk.

A “spherical of beneath regular temperatures within the Japanese Half late within the six- to 10-day interval will probably be a quick incidence, as situations shortly rebound hotter within the 11- to 15-day,” Maxar mentioned. “This comes out forward of one other spherical of troughing into the West, together with a lot belows at occasions within the Southwest, the place the forecast is colder than earlier.

“Alternatively, the forecast is hotter than earlier within the Japanese Half, the place above regular temperatures are favored. This contains an growing protection of a lot aboves into mid-period.”

‘Constant Promoting Stress’ Forward?

Nymex futures continued to flounder in the course of the Feb. 2-8 buying and selling interval. Modest internet features in Monday’s and Tuesday’s periods preceded an 18.8-cent selloff for the March contract on Wednesday.

The entrance month managed to claw again 3.4 cents to settle at $2.430 Thursday following a surplus-shrinking 217 Bcf withdrawal within the newest Power Info Administration (EIA) storage report. The storage print additionally missed to the bullish aspect of pre-report surveys.

The March contract climbed additional in Friday’s session, finally settling 8.4 cents increased at $2.514 to shut out the week.

Complete Decrease 48 storage stood at 2,366 Bcf as of Feb. 3, a 5.2% surplus to the five-year common, in accordance with EIA.

Regardless of the supportive end in the newest EIA information, the storage cushion is poised to develop considerably by the tip of February, in accordance with EBW Analytics Group.

This factors to “constant promoting strain” forward, EBW analyst Eli Rubin mentioned in a latest be aware to purchasers.

Current weather-adjusted balances present notable oversupply, although there stay doubtlessly supportive developments on the demand aspect as winter attracts to a detailed, in accordance with the analyst.

“Even after adjusting for blowtorch climate, January 2023 was 2.9 Bcf/d looser versus 10-year balances,” Rubin mentioned. “As Freeport LNG returns and coal-to-gas switching rises, nevertheless, a considerable 4.0 Bcf/d increase to weather-normalized demand paired with decelerating manufacturing development could lay the groundwork for a modest restoration in pure gasoline futures into the spring.”

In associated information, the Federal Power Regulatory Fee on Thursday granted Freeport LNG Improvement LP’s request to renew loading cargoes from one dock. Whereas the plant has not been cleared to restart operations, the approval is one in a collection that should happen earlier than manufacturing and shipments could resume after an explosion and hearth final June, which knocked the ability offline.

In the meantime, complete U.S. energy technology declined 7% 12 months/12 months in January, with totals in step with the three-year common, in accordance with analysts at Tudor, Pickering, Holt & Co. (TPH).

Pure gasoline technology rose 2% 12 months/12 months for the month, seeing its share of thermal technology complete round 66%, in step with 4Q2022 and up 8% 12 months/12 months, the agency estimated.

“Regionally, gasoline’ share of thermal technology improved versus 4Q2022 in two-thirds of our 12 tracked areas (excluding New York) with the Southeast and Texas trending most improved at plus-five and plus-four share factors, respectively,” the TPH analysts mentioned.

“For renewables, complete technology fell to round 69 TWh (minus 2% 12 months/12 months), with hydro (down 10% 12 months/12 months) and photo voltaic (down 3% 12 months/12 months) the laggards, whereas wind ticked up modestly (plus-2% 12 months/12 months).”

[ad_2]

Source_link

{kind=link}