[ad_1]

Investments in floating liquefied pure gasoline (FLNG) manufacturing terminals are poised to extend sharply within the subsequent 4 years, pushed by Europe’s have to displace Russian pure gasoline imports and Asia’s ongoing shift away from coal, in line with an evaluation from Westwood World Vitality Group.

Market analysis agency Westwood expects 18.3 million metric tons/12 months (mmty) of extra floating liquefaction services to come back on-line by 2027. That may signify an engineering, procurement and building (EPC) award worth of $13 billion, in line with Westwood’s Mark Adeosun, director of the agency’s PlatformLogix service, which covers mounted and floating manufacturing terminals worldwide.

“With growing power demand and the challenges of power safety, the necessity for gasoline to satisfy instant and medium-term power demand is driving investments within the FLNG market,” Adeosun stated.

Past 2027, Westwood expects one other 36.5 mmty of FLNG services to enter service, representing an EPC worth of $22 billion.

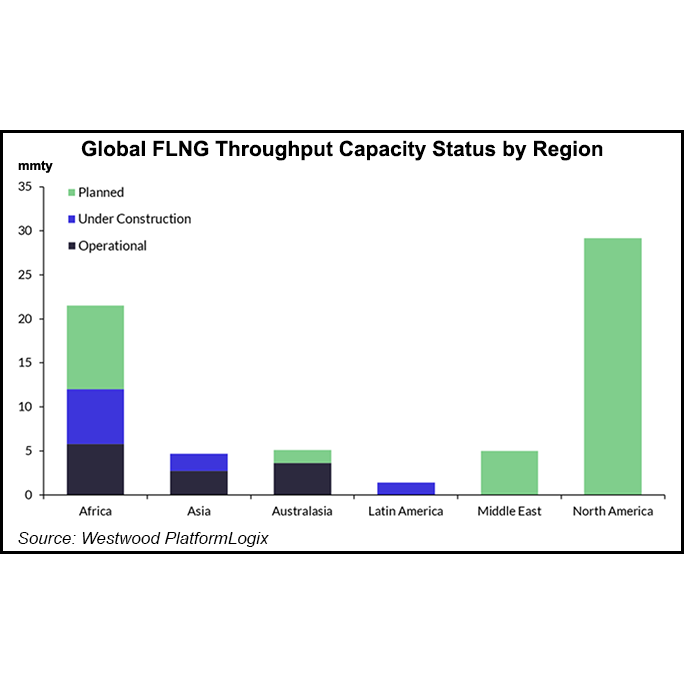

Till now, FLNG improvement has been sluggish. Since Shell plc introduced a remaining funding determination (FID) on its 3.6 mmty Prelude FLNG vessel offshore Australia 12 years in the past, solely 5 models with 12 mmty of capability have entered service globally.

“The challenges surrounding Prelude have been well-documented, together with building delays, price overruns and ongoing operational challenges, whereas weakened market circumstances halted extra funding from the supermajor,” Adeosun stated.

Whereas a number of FLNG initiatives that had been into account did not progress to FID, others are gaining steam amid a push to construct extra infrastructure following Russia’s invasion of Ukraine, which upended world power flows.

LNG import capability in Europe alone is poised to leap by 34% from 2021 ranges, or by 6.8 Bcf/d within the subsequent two years, in line with the U.S. Vitality Info Administration.

FLNG initiatives may be constructed quicker and at decrease prices than bigger baseload liquefaction terminals onshore. In addition they will help in creating stranded gasoline belongings.

Westwood famous that the offshore FLNG provide push can be led by North America, which can be a pacesetter in onshore terminals.

Delfin Midstream Inc.’s plans to put in 4 floating vessels offshore Louisiana might produce as much as 13.3 mmty. The corporate has not but sanctioned the undertaking, however it’s focusing on service round 2026.

In the meantime, in Canada, one other three initiatives are deliberate that would create 17.5 mmty of FLNG capability. Nonetheless, Adeosun stated Westwood doesn’t anticipate any Canadian initiatives to start out industrial manufacturing earlier than 2028.

Close to-term, Westwood expects Africa to account for 56%, or 10.2 mmty, of the FLNG capability anticipated to come back onstream between 2023 and 2027. There are 4 FLNG models at present underneath building or being reactivated for the area.

“The usage of FLNG models to develop large gasoline reserves offshore Mauritania, Senegal, Tanzania and Mozambique can be perceived to be extra favorable in comparison with onshore alternate options, because it represents a lesser safety danger” to worldwide oil corporations, Adeosun stated.

Elsewhere, New Fortress Vitality Inc. has plans to host liquefaction crops on transformed jack-up rigs and glued platforms internationally. The primary so-called Quick LNG terminal is predicted to provide its first LNG this summer season offshore Altamira, Mexico.

Different FLNG models are being thought-about offshore Israel and Australia.

Adeosun cautioned that LNG provide progress is predicted to be strong within the coming years, notably in america and Qatar, which might create the danger of an oversupply and push some larger price initiatives out of the market.

“Because of this FLNG improvement should deal with its differentiator to compete – together with its velocity to market and suppleness,” he stated.

[ad_2]

Source_link

{kind=link}