[ad_1]

Beleaguered pure gasoline futures fell a second day, hampered once more by strong provides and weakening weather-driven demand. The April Nymex gasoline futures contract misplaced 5.8 cents day/day and closed at $2.030/MMBtu. Might futures settled at $2.147, down 6.8 cents.

At A Look:

- Entrance month loses 5.8 cents

- Demand poised to ease

- Provides stay elevated

NGI’s Spot Fuel Nationwide Avg. slipped 9.5 cents to $2.470.

Manufacturing held above 100 Bcf/d on Tuesday, on par with the beginning of the week and up to date peak ranges. On the similar time, Nationwide Climate Service (NWS) forecasts Tuesday pointed to hotter situations than in earlier outlooks, with benign situations anticipated throughout the South – and in some northern markets — late this week and subsequent, minimizing demand.

“Because of heavy end-of-season pure gasoline provides and little climate, Nymex natty bears confirmed no compunction to take cash off the desk earlier than the quarter ends,” mentioned analysts at The Schork Report.

The April contract rolls off the books with Wednesday’s settlement, when Might turns into the entrance month. Buying and selling into expiry is commonly uneven, famous Mizuho Securities USA LLC’s Robert Yawger, director of power futures. He’s awaiting futures to check the sub-$2 degree earlier than that.

“There’s a probability the roll can save pure gasoline from sliding over the $2 cliff” if Might futures “can simply dangle in there till after” expiration, Yawger mentioned.

Analyst Brian LaRose of ICAP Technical Evaluation echoed that sentiment. “Watching intently for any indicators that the bulls may be capable of discover their footing as we head into the tip of the month,” he mentioned.

In bulls’ favor, LNG feed gasoline demand on Tuesday hung round report ranges close to 13.9 Bcf/d, based on EBW Analytics Group. The agency cited the continued restoration of a key Texas liquefied pure gasoline export plant. Freeport LNG, compelled offline in June following a fireplace, is within the means of constructing again to almost 2.4 Bcf/d of capability. Nominations at Freeport approached 1.6 Bcf on Tuesday.

[Decision Maker: A real-time news service focused on the North American natural gas and LNG markets, NGI’s All News Access is the industry’s go-to resource for need-to-know information. Learn more.]

Asian and European requires U.S. LNG are anticipated to carry sturdy and probably surge forward of subsequent winter, given restricted home provide sources on every continent. Europe, particularly, continues to grapple with long-term plans to fill the void left by diminished pipeline provides from Russia amid the Kremlin’s conflict in Ukraine.

Stout Provides

Following transient rashes of late-winter climate round mid-March, analysts anticipate a second consecutive bullish U.S. Vitality Data Administration (EIA) storage print this Thursday.

Early draw estimates submitted to Reuters for the week ended March 24 averaged 55 Bcf. NGI modeled a draw of 57 Bcf. That compares with a five-year common decline of 17 Bcf.

EIA reported a withdrawal of 72 Bcf for the March 17 interval. It in contrast with a five-year common decline of 45 Bcf. The lower lowered inventories to 1,900 Bcf.

Nonetheless, even steep late-season storage pulls are unlikely to place a major dent into surpluses relative to current historical past. Shares as of March 17 had been far above the year-earlier degree of 1,396 Bcf and the five-year common of 1,549 Bcf.

On the similar time, the specter of financial recession threatens to curb industrial demand within the months forward. The monetary disaster created by the failures of Silicon Valley Financial institution and Signature Financial institution earlier this month – and the downfall of Credit score Suisse in Europe – may drive banks to tug again on lending. When companies lack entry to credit score, spending falls and downturns are extra probably, mentioned Rupert Thompson, chief economist at Kingswood Group.

The banking sector “remained the focal point and markets remained in a skittish temper,” Thompson mentioned Tuesday. “The financial outlook stays murky to say the least and is ready to stay so for a very good few months.”

Tender Spot Costs

Bodily costs principally traded in a slender vary of features and losses, relying on the area, however the nationwide common swung decrease on declines within the risky West.

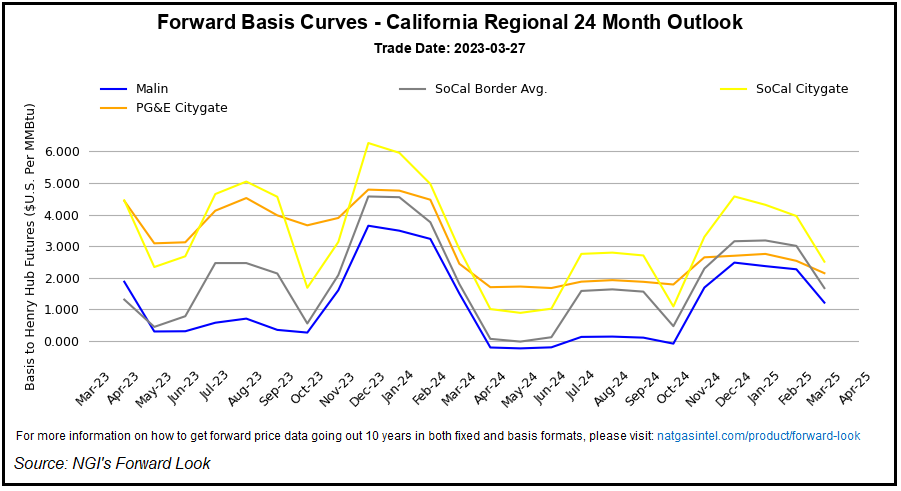

Malin shed 21.0 cents day/day to common $5.665, whereas PG&E Citygate fell 16.5 cents to $6.665 and Northwest Sumas dropped 75.5 cents to $2.995.

NWS information confirmed a number of climate methods monitoring throughout the nation through the present buying and selling week, delivering chilly air to the Mountain West and northern reaches of the Plains. Some cooler temperatures are projected to drop additional south, although that is more likely to go away gentle situations from Texas to Florida.

For subsequent week, forecasts present related situations permeating the US.

Maxar’s Climate Desk on Tuesday mentioned warmer-than-normal temperatures would span japanese parts of the Decrease 48 for a lot of the next 15 days.

“On the peaks, temperatures are forecast within the upper-80s for Dallas and Houston on days seven and eight, mid-60s in Chicago on day eight and mid- to upper-70s in Washington, DC, from days eight by way of 10,” Maxar mentioned.

In the meantime, on the upkeep entrance, El Paso Pure Fuel Pipeline mentioned that, from Tuesday by way of the tip of March, it might conduct cleansing and sensible device runs by way of its Line 1100 in Texas, slicing as much as 94 MMcf/d of westbound flows.

Wooden Mackenzie analyst Quinn Schulz famous that different upkeep initiatives and circulation disruptions have hampered the supply of gasoline from the Permian Basin to western markets, impacting provides and placing upward strain on spot costs within the Southwest and Southern California.

Nevertheless, within the Southwest Tuesday, KRGT Del Pool misplaced 44.0 cents to $5.445, whereas SoCal Border Avg. fell 96.0 cents to $4.615.

[ad_2]

Source_link

{kind=link}