[ad_1]

The Worldwide Vitality Company (IEA) anticipates that worth volatility and intense competitors over LNG volumes may warmth up once more this yr regardless of months of falling costs, however the outlook remains to be “extremely unsure,” particularly relating to Chinese language demand.

Europe’s rush to fill winter storage and exchange Russian pipeline flows final yr with expensive liquefied pure gasoline cargoes was aided partly from China’s relative absence from the spot market. Analysts have been warning since final fall that the tip of Covid restrictions in China may result in it retaking its place because the world’s high importer, triggering extra worth spikes and dwindling European provide.

Nonetheless, Chinese language importers have continued to belay an uptick in spot purchases, clouding the IEA’s forecast for the nation’s LNG demand.

“China is the nice unknown in 2023,” IEA’s Keisuke Sadamori, director of vitality markets and safety, stated. “If world LNG demand returns to pre-crisis ranges, that may solely intensify competitors on world markets and inevitably push costs up once more.”

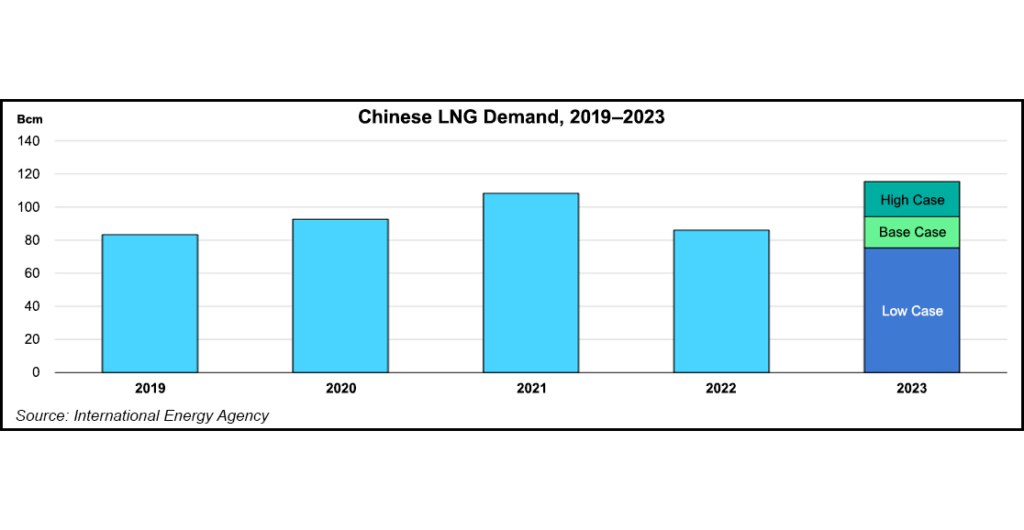

Within the IEA’s first world gasoline market report of the yr, researchers advised China’s home LNG demand may enhance this yr, however eventualities ranged from 10-35%. If world LNG costs proceed to fall and China’s financial exercise will increase, fierce competitors for volumes may return together with costs at “unsustainable ranges.”

IEA additionally modeled a state of affairs the place LNG demand may proceed to say no by 12%, or 10 billion cubic meters (Bcm), however that was thought of unlikely. The vary of uncertainty for China’s LNG demand was round 40 Bcm, falling to 75 Bcm on the low finish and reaching 115 Bcm on the excessive finish.

Compared, the vary of uncertainty for Europe’s future provide of pipeline gasoline from Russia is smaller at 28 Bcm.

Chinese language LNG imports fell from virtually 80 million tons (Mt) in 2021 to 64 Mt final yr, in keeping with knowledge from Kpler. Month-to-month Chinese language imports have been underneath 2021 averages because the starting of the yr, with 6 Mt imported in January and 5 Mt imported in February.

China’s gasoline consumption fell by 1% final yr, the primary annual decline in 4 a long time, in keeping with IEA. Many of the drop was attributed to the facility sector, which noticed giant will increase in each renewable technology and coal use.

Gasoline consumption is estimated to rebound by 7% this yr, led by will increase in demand from business. Nonetheless, IEA researchers famous it doesn’t essentially imply a rise in China’s demand for spot market targets.

Together with will increase in home manufacturing and above common gasoline storage ranges, China has continued to prioritize its long-term LNG contracts. IEA researchers advised China may enhance its LNG imports this yr to 2021 ranges with out rising spot purchases due to an uptick in contract volumes.

“With about 13 Bcm of recent LNG contracts beginning supply in 2023, China’s contracted LNG quantity is heading in the right direction to achieve practically 110 Bcm this yr, considerably greater than projected LNG demand in all however essentially the most optimistic eventualities (and barely greater than China’s complete LNG imports at their 2021 peak of 108 Bcm),” researchers wrote. Asia’s gasoline consumption as a complete decreased by 2% final yr, in keeping with IEA. Excessive world costs inspired an uptick in coal-fired technology, whereas giant importers like Japan and Korea constructed gasoline reserves. Asian gasoline demand this yr is predicted to rise 3%, led by recoveries in China and India, however it’s anticipated to be nicely under peak 2019 ranges.

[ad_2]

Source_link

{kind=link}