[ad_1]

A yr after Russia’s invasion of Ukraine splintered the vitality panorama in Europe, the area is constant to diversify its pure fuel provide, thanks partially to a wave of LNG imports. Nonetheless, it nonetheless faces years of potential shortages as world export capability stays tight.

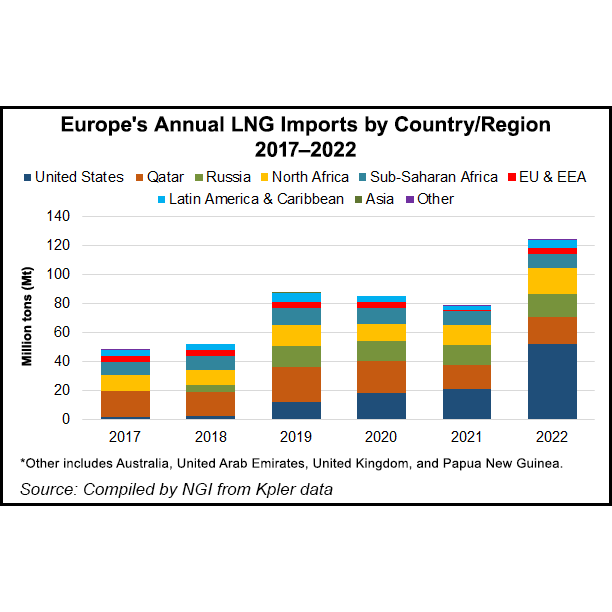

Since final February, liquefied pure fuel imports have taken the highlight as a balancing pressure for Europe’s pure fuel provide as international locations moved to staunch the influence of dwindling Russian pipeline fuel. LNG flows to Europe almost doubled, leaping to 106.44 million tons (Mt) final yr in comparison with 68.26 Mt in 2021, in keeping with information from Kpler.

Whereas allied partnerships helped LNG imports enhance exponentially, the super-chilled gas made up about 25% of Europe’s fuel provide by final November. Throughout the identical timeframe, the area nonetheless relied on a mix of Russian pipeline fuel and LNG for about 25% of the availability share. In 2021, Russian pipeline fuel made up virtually 50% of the continent’s provide.

[2023 Natural Gas Price Outlook: How will the energy industry continue to evolve in 2023? NGI’s special report “Reshuffling the Deck: High Stakes for Natural Gas & The World is All-In” offers trusted insight and data-backed forecasts on U.S. natural gas and the global LNG markets. Download now.]

Europe might proceed to see risky costs and infrastructure bottlenecks for the following a number of years, however Kpler LNG analyst Ana Subasic mentioned it’s clear that LNG is predicted to proceed “main the change within the provide construction for European fuel,” with exports anticipated to exceed final yr’s document ranges.

“At massive, Kpler Perception expects European LNG provide will enhance by 11% y/y to 138 Mt imported in 2023,” Subasic instructed NGI.

As Russian flows dwindled final yr, Norway turned the biggest pure fuel pipeline provider to Europe, adopted by Algeria, in keeping with information from the European Fee. Producers working in Norway, like Equinor ASA, have been planning long-term investments to spice up output for the following a number of years to extend exports to western Europe.

Nonetheless, Subasic instructed NGI that, “Norwegian exports to Europe could have restricted progress throughout its heavy upkeep interval scheduled for this summer season.” Further volumes from Algeria are additionally anticipated to be restricted within the short-term. In the meantime, the remaining pipeline exports to Europe from Russia might drop additional by an estimated 36-39 billion cubic meters (Bcm), or as much as 1.4 Tcf, by the top of the yr, Subasic mentioned.

African LNG Development

With a tough cap on the expansion of pipeline provide to Europe, the area should depend on rising LNG capability to stability potential elevated competitors with Asia. Nonetheless, cargoes from new tasks beginning up in 2023 will likely be restricted, because the yr is predicted to have the bottom addition to world export capability in a decade.

A lot of the additions to export capability through the yr are anticipated to return from Africa. The 0.3 Bcf/d Higher Tortue Ahmeyim LNG mission operated by BP plc offshore Mauritania and Senegal and the Tango Floating LNG manufacturing unit situated offshore the Republic of Congo (0.1 Bcf/d) might begin up this yr.

Africa turned a rising supply of LNG for Europe final yr, with the area receiving its first cargoes from Cameroon through the yr and elevated volumes from Equatorial Guinea and Angola.

Nigeria, Africa’s largest exporting nation, noticed a drop in total output attributable to safety considerations and catastrophic flooding, limiting exports to Europe final yr. In the meantime, Egypt greater than doubled its exports to Europe to five Mt because it obtained extra feed fuel from Israel and different Mediterranean fuel producers to fulfill demand.

Egyptian Power Minister Tarek el-Molla reportedly instructed attendees on the Egyptian Petroleum Present on Feb. 15 that the federal government expects LNG output to be maintained at heightened ranges, probably reaching 7 Mt for the yr. He added that Egypt is exploring methods to extend utilization and broaden capability on the nation’s two LNG crops.

European Union Power Commissioner Kadri Simson, who additionally spoke on the present, mentioned Egypt could have a rising function as “a regional fuel hub” because the EU launches its joint fuel shopping for scheme. Known as the EU Power Platform, Simson mentioned the bloc goals to buy 13.5 Bcm (477 Bcf) of fuel with a give attention to LNG cargoes.

“LNG markets are the primary goal of our scheme, and it goes with out saying that it is a vital alternative to strengthen our vitality ties even additional,” Kadri mentioned.

Extra volumes can also hit the market in Asia through the yr, serving to stability world provide. A 3rd practice at Tangguh LNG (0.5 Bcf/d) in Indonesia, additionally operated by BP, might enhance the power’s capability by 50% someday within the first half of the yr.

Whereas prolonged outbreaks of Covid-19 after China ratcheted down its containment insurance policies have helped lengthen the nation’s break from the spot market, Subasic mentioned the main LNG purchaser nonetheless presents the “greatest draw back danger” for Europe outdoors of unplanned outages. Nonetheless, elevated Chinese language exercise could possibly be offset by an anticipated decline in demand from Japan and Korea.

Regasification and Restarts

A big portion of the LNG provide progress anticipated within the yr might additionally come from the restart of the Freeport LNG facility in Texas. As soon as the two.38 Bcf/d facility ramps as much as full capability, probably someday within the spring, a further 5.6 Mt could possibly be out there to the worldwide market by way of 2023, in keeping with Kpler. A few of these returning volumes are beneath contract to companies together with Uniper SE, BP and South Korea’s SK Group.

LNG producers in the US led the surge in volumes for Europe throughout 2022, contributing 52.86 Mt final yr, or roughly 50% of the continent’s LNG provides.

Europe might additionally profit from a full yr of manufacturing from Equinor ASA’s Hammerfest LNG in Norway. The ability got here again on-line final June after virtually two years of repairs following a fireplace. This yr may even mark the primary full yr of manufacturing for Enterprise International LNG Inc.’s Calcasieu Cross facility in Louisiana.

Whereas the inflow of LNG cargoes throughout 2022 helped Europe retailer above common volumes of pure fuel earlier than the winter, inadequate regasification capability led to bottlenecks and worth volatility through the top of the restocking season.

International locations throughout Europe rushed to put in floating storage and regasification models (FSRU) through the yr and extra are anticipated to return on-line in 2023. European import capability might attain 5.3 Bcf by the top of 2023, in keeping with the Worldwide Group of Liquefied Pure Gasoline Importers.

By the top of the yr, Kpler expects France so as to add 0.4 Bcf/d of regasification capability utilizing an FSRU vessel referred to as Cape Anne at Le Havre port. The FSRU is predicted to return on-line within the fall of 2023.

Italy can be anticipated to launch its first FSRU on the port of Piombino someday through the spring. Snam SpA leased an FSRU terminal vessel referred to as Golar Tundra, which is predicted so as to add 0.5 Bcf/d of capability. By the top of the yr, Germany might add a further two FSRUs to its community of three terminals already working.

[ad_2]

Source_link

{kind=link}