[ad_1]

Pure fuel futures churned out one other worth acquire on Tuesday, with analysts largely seeing the transfer increased as technically pushed somewhat than fueled by any important change within the provide/demand stability. The March Nymex fuel futures contract climbed 12.7 cents on the day to $2.584/MMBtu, whereas April futures picked up 12.9 cents to $2.664.

At A Look:

- Little chilly in February forecast

- Oversupply seen by means of 2023

- Money up, however Line 2000 returns

Spot fuel costs strengthened as properly, with NGI’s Spot Fuel Nationwide Avg. up 14.5 cents to $2.660.

Uncommon because it was in current weeks, Tuesday’s almost 13-cent bounce on the entrance of the Nymex curve gave the impression to be a wake-up name for sleepy bulls who’ve grown weary of the continued balmy February outlook, robust manufacturing ranges and wholesome underground storage inventories which have led to the regular sell-off alongside the futures curve. Positive, there’s Freeport LNG’s impending return, however even that added demand could also be priced into the market and isn’t more likely to pack the identical punch immediately as it could have a few months in the past.

As a substitute, grumblings that the availability aspect could also be set to rethink development plans for the rest of the 12 months transfer to middle stage for the fuel market, in response to Mobius Threat Group.

With fuel costs coming off some 60% this winter, whether or not the entrance of the curve has sufficiently moved to restrict any provide aspect additions is the query at hand, the Houston agency stated.

A take a look at the Nymex strip reveals sub-$3 pricing by means of a lot of the summer season earlier than a bounce in July. What’s extra, costs stay above the $3 all through 2024, doubtless because of new liquefied pure fuel capability scheduled to enter the market throughout that point.

Nevertheless, as Mobius famous, the again of the curve is “wandering round with the competing forces of demand-side additions in 2024 countered by will increase in producer hedging exercise.”

Goldman Sachs additionally tackled the problem of (over)provide in a current be aware to purchasers.

The Goldman analyst crew, led by Umang Choudhary, stated that whereas the fuel market could profit from some coal-to-gas switching demand at these decrease fuel worth ranges, U.S. fuel producers could have to restrict exercise and shift to manufacturing declines earlier than accounting for the good thing about added demand from the facility era sector.

Fuel producers historically have responded to decrease implied fuel costs with a three-month lag to exercise cuts, in response to Goldman. This interprets into manufacturing with a roughly six-month lag. To maintain manufacturing largely flat throughout key dry fuel basins, Goldman analysts stated a discount within the rig depend of round 25-30 is required to stability the market. In addition they suggested that producers could contemplate fewer properly completions.

This decline could be pushed largely from the Haynesville Shale, the place the Goldman analysts stated a roughly $3.25 fuel worth is required to generate 10% returns. To maintain manufacturing flat, they counsel a rig depend discount of about 15-20 rigs and completions of round 60 wells/month.

There are dangers to the Goldman view, nevertheless.

The agency stated it assumes a “rational” manufacturing response given expectations for public producer self-discipline with a give attention to returns/free money movement, and more durable borrowing circumstances for the personal operators. Nevertheless, the present tight oilfield providers market “can restrict producers’ capability to be extra conscious of immediately’s costs,” in response to Goldman.

[Decision Maker: A real-time news service focused on the North American natural gas and LNG markets, NGI’s All News Access is the industry’s go-to resource for need-to-know information. Learn more.]

As well as, a ample drilled and uncompleted properly backlog within the Haynesville could pose a danger if robust completions exercise continues whilst rigs are dropped, the agency stated. The Goldman crew additionally sees danger coming from much less disciplined habits amongst fuel producers provided that 2024-25 Nymex strip costs are nonetheless above $3.50. This, together with addition of hedges, can cut back the scale of producer response wanted to stability the market, analysts stated.

For its half, the Vitality Info Administration (EIA) revised decrease its Henry Hub worth outlook for 2023, modeling a median worth of $3.40. This can be a decline of 30% versus the company’s predictions just one month in the past.

Within the newest Quick-Time period Vitality Outlook, printed Tuesday, the EIA estimated that U.S. dry pure fuel manufacturing would common 100.2 Bcf/d in January, a brand new document. Manufacturing is on monitor to common 100-101 Bcf/d this 12 months, the company stated.

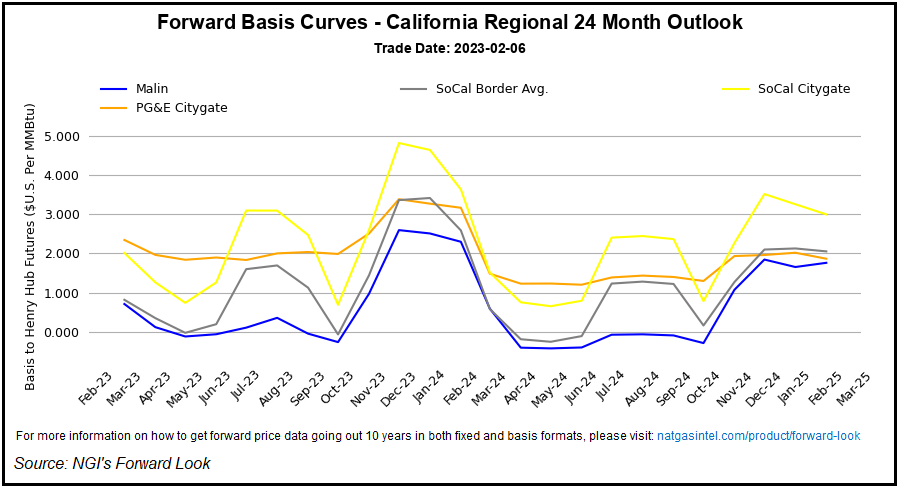

Money Up, Good Information For West

Spot fuel costs additionally recovered Tuesday, led by the West Coast, the place moisture will stream forward of and alongside a chilly entrance to drive up fuel demand.

The Nationwide Climate Service (NWS) stated heavy snow was anticipated within the increased elevations of the Cascades and northern Rocky mountains into Wednesday. By Wednesday night time, the chilly entrance ought to emerge within the Plains and proceed to push southeastward.

“Cooler air within the wake of the entrance will end in max temperatures briefly dropping 5-10 levels beneath common,” NWS forecasters stated.

Stress was forecast to construct over the West behind the entrance, whereas the subsequent frontal system might method the coastal Pacific Northwest late Thursday or early Friday, in response to NWS.

As for costs, the SoCal Border Avg. tacked on 40.0 cents day/day to common $4.445 for Wednesday’s fuel movement. El Paso S. Mainline/N. Baja money was up 37.0 cents to $4.475, whereas within the Rockies, Opal was up 17.0 cents to $3.940.

Even with the biggest day/day worth will increase within the nation, the beneficial properties on the West Coast are solely a fraction of the gargantuan spikes seen earlier within the winter. What’s extra, there’s been a serious constructive improvement that ought to additional alleviate a few of the volatility seen within the area this season.

El Paso Pure Fuel Pipeline (EPNG) late Monday acquired authorization from the Pipeline and Hazardous Supplies Security Administration to totally elevate the continued stress restriction on Line 2000. This line had restricted 550,000 MMcf/d of westbound flows since Aug. 15, 2021, following an explosion.

In a discover, EPNG famous that, though stress has returned, the drive majeure stays in impact and is predicted to formally conclude on Feb. 15. EPNG, nevertheless, has begun its restart plan to return Line 2000 to industrial service.

Along with bringing elevated provide to western markets, and theoretically decrease costs, the return of Line 2000 might also deliver reduction to Waha costs upstream within the Permian Basin. With pipeline capability tapped out, the rise in throughput might assist assist costs within the area, particularly during times of low demand just like the upcoming spring shoulder season.

On Tuesday, Waha money averaged $1.620, up 32.5 cents on the day, which was typically in keeping with worth will increase seen all through the remainder of the nation.

[ad_2]

Source_link

{kind=link}