Ocean transport demand is historically measured in “ton-miles”: volumes multiplied by distance. So, right here’s a paradox: Ton-miles for liquefied pure fuel transport have fallen in 2022, as a result of most cargoes from the U.S. are being pulled to war-stricken Europe as a substitute of going longer-haul to Asia. And but, LNG transport spot charges have skyrocketed to Guinness Ebook ranges of as much as $500,000 per day.

How is that this doable?

This paradox was addressed on the Marine Cash New York Ship Finance Discussion board on Thursday. The reply — which affords an necessary lesson on understanding demand in all transport segments, from tankers to bulkers to container ships — is that it’s not all about ton-miles.

Ton-days not ton-miles

There are two the explanation why LNG transport spot charges have gone by way of the roof regardless of falling ton-miles: the impact of time or “ton-days” (quantity multiplied by voyage time) and the impact commodity pricing on ship availability.

Jefferson Clarke, head of LNG industrial analytics at Poten & Companions, stated on the Marine Cash occasion, “After we forecast transport supply-demand balances, it’s not truly nearly ton-miles. Whereas that’s an necessary aspect, we additionally concentrate on the influence of time.”

Brokerage BRS highlighted this problem in a dry bulk transport report earlier this yr. “For the uninitiated, freight demand is usually perceived to be absolutely the quantity of cargo loaded and shipped. A transport skilled … is aware of {that a} cargo that traveled throughout half the globe goes to generate extra demand for freight capability [i.e., ton-miles].”

However “whereas ton-miles have been extensively used within the transport trade, one hidden flaw is that it doesn’t keep in mind ready time,” wrote BRS. “Therefore, it is going to be instructive to [reexamine] freight demand utilizing ton-days.”

The runup in charges for bigger dry bulk ships in 2021 was closely pushed by Chinese language port delays that boosted ton-days. Surging container-ship freight charges from Asia to the West Coast in late 2021 have been partly pushed by unloading delays in Los Angeles/Lengthy Seashore. The increase in very giant crude service (VLCC) charges in spring 2020 was pushed by floating storage, vastly extending the time between loading and discharge.

That very same dynamic is now taking part in out in LNG transport.

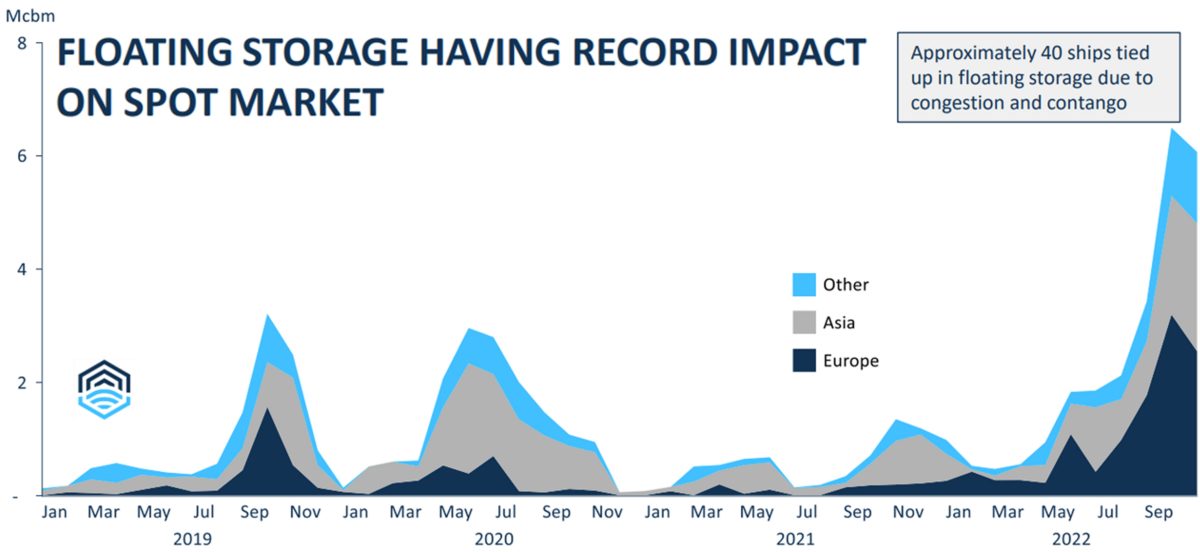

Flex LNG (NYSE: FLNG) CEO Oystein Kalleklev stated on a quarterly name final Tuesday, “There’s a enormous buildup of [LNG] ships tied up in floating storage, particularly in Europe but additionally in different nations. As of at the moment, we’re at an all-time excessive stage of round 40 ships being tied up in floating storage, which is taking out loads of ships from the final freight market, which is making the freight market very tight.”

Looming insurance coverage ban on Russian crude

This identical ton-days issue is predicted to be a key constructive crude-tanker spot charge driver when the EU and U.Ok. ban on transport insurance coverage for Russian crude exports comes into impact in two weeks.

Larger voyage distance — ton-miles — would be the largest issue, however not the one issue.

Wintertime Russian exports from northern ports are anticipated to be dealt with by smaller ice-class tankers that will likely be compelled to conduct time-consuming ship-to-ship transfers with bigger tankers, doubtless off the coast of Africa. Tankers loading Russian crude within the Black Sea might additionally face transit delays as insurance coverage is vetted previous to passage by way of the Bosporus Strait.

Contango and ton-days

Spot transport charges are pushed by commodity costs in not less than two methods. First, associated to ton-days, if the ahead commodity worth is excessive sufficient versus the present worth (often known as contango) to induce floating storage. Second, if the arbitrage earnings — the worth distinction between one area and one other — are exceptionally excessive.

The contango in crude pricing brought on the VLCC charge spike in spring 2020, growing ton-days. LNG costs in Europe are in contango now.

Kalleklev stated on the Marine Cash discussion board, “Not solely do we now have all this congestion in Europe, however there’s a glut of LNG coming into Europe, pushing immediate costs decrease, which means you get this massive contango. Immediately, there are two incentives for floating storage, congestion and contango, so charges have skyrocketed.”

Commodity worth impact on constitution markets

The second commodity-price issue — arbitrage earnings between areas — appears much more necessary to at the moment’s LNG spot charges, on account of its impact on the long-term constitution market.

In any spot transport market, the speed will depend on what number of vessels are literally out there for spot enterprise. LNG ships out there for short-term employment are actually just about nonexistent as a result of they’re all on long-term charters and people charterers are usually not subletting their vessels into the spot commerce.

LNG commodity costs have hit file highs this yr within the wake of the Ukraine-Russia warfare. At one level, pure fuel in Europe was priced on the equal of $600 per barrel of oil, stated Francisco Blanch, head of world commodities at Financial institution of America.

In line with Clarke, “Within the present setting, LNG [commodity] costs are extra a figuring out issue on transport demand.”

Clarke defined: “Charterers are holding onto tonnage and never subletting their vessels out. They’re extra involved about accessing tonnage. They’re extra targeted on the [long] time period market than the spot market. So, after we learn these headlines of excessive [spot] charges, they’re largely irrelevant, as a result of there’s little or no liquidity.”

In different phrases, LNG ship charterers can make more cash by pocketing arbitrage earnings transferring their very own cargoes than from briefly subletting their vessels to others. As a result of there are so few ships left for spot buying and selling, LNG spot transport charges have risen to $450,000 to $500,000 a day on account of lack of tonnage — however only a few vessel house owners truly earn these charges.

“It’s not likely a market,” stated Kalleklev of the present spot LNG transport enterprise.

Parallel in container-ship leasing

This excessive emphasis on long-term charters doesn’t happen in dry bulk and oil tanker trades, as a result of possession is very fragmented, many house owners maintain a considerable portion of their fleets on spot even in increase occasions, and tankers are bulkers are largely in “tramp” trades (i.e., no fastened port pairs).

However there was a latest parallel in container-ship leasing.

In 2021 and the primary half of 2022, container-ship house owners selected to lease out tonnage on traditionally profitable multiyear offers. Liners agreed to pay exceptionally excessive charges for prolonged durations. Just about each ship out there for lease was leased out.

As in LNG transport, container-ship house owners opted for long-term offers over short-term ones despite the fact that short-term charges have been a lot greater, as a result of a fowl within the hand is price greater than two within the bush. In the meantime, liners didn’t sublet the ships they chartered, as a result of they might earn far more utilizing the chartered ship to move containerized cargo than they might from sublet revenue.

This severely restricted container-ship tonnage out there for short-term, multi-month charters, inflicting short-term leasing charges for a really small variety of vessels to spike to $200,000 per day.

Add all of it up and the takeaways are: For LNG transport and container-ship leasing, concentrate on long-term charges, not the short-term charges that get the headlines, and for all transport markets, suppose much less about ton-miles and extra about ton-days, which embody not solely voyage size but additionally loading and unloading delays.

Click on for extra articles by Greg Miller

Associated articles:

[ad_2]

Source_link

{kind=link}