[ad_1]

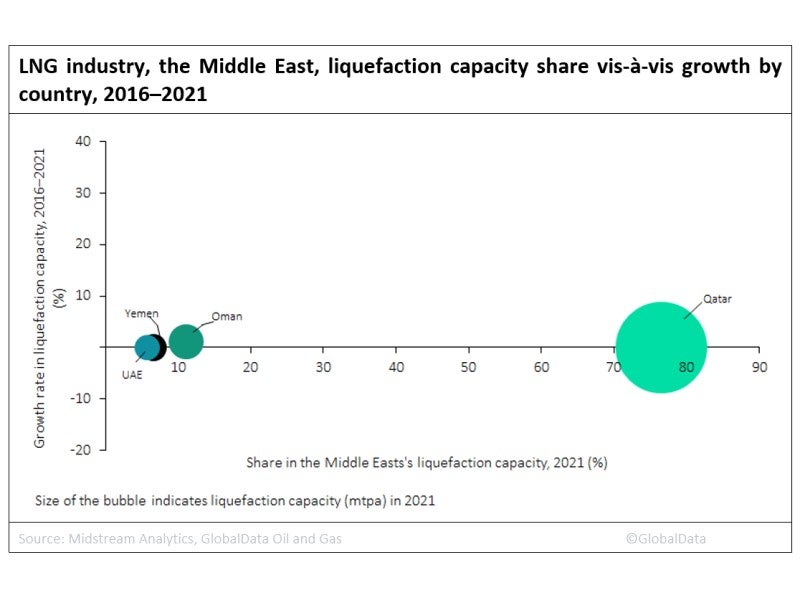

GlobalData’s newest report, ‘International LNG Business Outlook to 2026 – Capability and Capital Expenditure Outlook with Particulars of All Working and Deliberate Terminals’, signifies that the full liquefaction capability of the Center East in 2021 was 101mtpa. The liquefaction capability within the Center East elevated from 100.8mtpa in 2016 to 101.3mtpa in 2021 at an AAGR of 0.1%. Qatar, Oman, Yemen and United Arab Emirates are the international locations within the Center East with lively liquefied pure fuel (LNG) liquefaction terminals in 2021.

Ras Laffan III (Qatar), Ras Laffan II (Qatar) and QatarGas I (Qatar) are the main liquefaction terminals of the Center East. These began operations in 2009, 2004 and 1996, respectively.

Within the Center East, Qatar leads amongst international locations with a liquefaction capability of 78mtpa in 2021, contributing to 76.5% of the Center East’s complete capability. Ras Laffan III, Ras Laffan II and Qatargas I are the main lively liquefaction terminals within the nation.

Oman ranks second within the Center East with a complete liquefaction capability of 11mtpa in 2021. Oman’s share within the Center East’s complete liquefaction capability was 11.2%. Oman and Qalhat are the 2 lively liquefaction terminals within the nation.

In 2021, Yemen stands third among the many Center East’s international locations with a contribution of 6.6% of the area’s complete liquefaction capability or 7mtpa. Yemen is the one operational terminal within the nation.

The United Arab Emirates follows Yemen with a capability of 6mtpa, contributing to five.7% of the Center East’s complete liquefaction capability. Abu Dhabi is the one lively liquefaction terminal within the nation.

[ad_2]

Source_link

{kind=link}