[ad_1]

Pure gasoline futures floundered again into freefall Wednesday – the case of a majority of buying and selling periods early within the new 12 months – as manufacturing climbed, benign climate continued and the market braced for an anemic storage withdrawal.

At A Look:

- Immediate month sheds 27.5 cents

- Manufacturing hits 102 Bcf/d

- Climate forecasts wobble

After a 16.7-cent achieve a day earlier, the February Nymex gasoline futures contract settled at $3.311/MMBtu on Wednesday, down 27.5 cents day/day. March shed 14.2 cents to $3.111.

NGI’s Spot Fuel Nationwide Avg. slid 18.5 cents to $5.930. It had climbed 90.5 cents on Tuesday.

Reflecting momentum gathered in 2022 following lofty home demand and calls from Europe for U.S. exports, manufacturing topped 102 Bcf/d in Bloomberg’s Wednesday estimate, placing it in keeping with file ranges.

Nevertheless, due to seasonally delicate climate throughout giant swaths of the nation – from the South to the East – to start out 2023, demand has tapered and costs have dropped greater than 50% from late final 12 months. Forecasts present a return of extra widespread winter climate within the last week of January, however the climate outlook has fluctuated each day and left merchants doubting the depth and length of the approaching chilly.

Each the American and European climate fashions marketed hotter traits in a single day for the ultimate week of January, based on NatGasWeather.

“In a single day information maintains very mild nationwide demand the subsequent three days, mild this weekend into the beginning of subsequent week, however nonetheless sturdy demand Jan. 26-31,” NatGasWeather mentioned Wednesday. Nevertheless, the outlook within the newest mannequin runs was “merely not as spectacular with the quantity of chilly into the U.S. and in addition not as aggressive in advancing subfreezing air into the southern and jap U.S.”

Forecasts wanted to take care of or strengthen chilly within the outlook for late January to keep away from “frustration/promoting” available in the market, the agency added.

StoneX Monetary Inc.’s Thomas Saal, senior vice chairman of vitality, echoed that sentiment.

“Mom Nature is fairly delicate proper now and with out a change, it’s trying like a comparatively heat winter,” Saal informed NGI. “Now, there’s quite a bit left of the season, however for probably the most half, the market is ready to see. And within the meantime, there’s loads of provide, and that’s weighing on costs.”

Storage, Freeport Wildcards

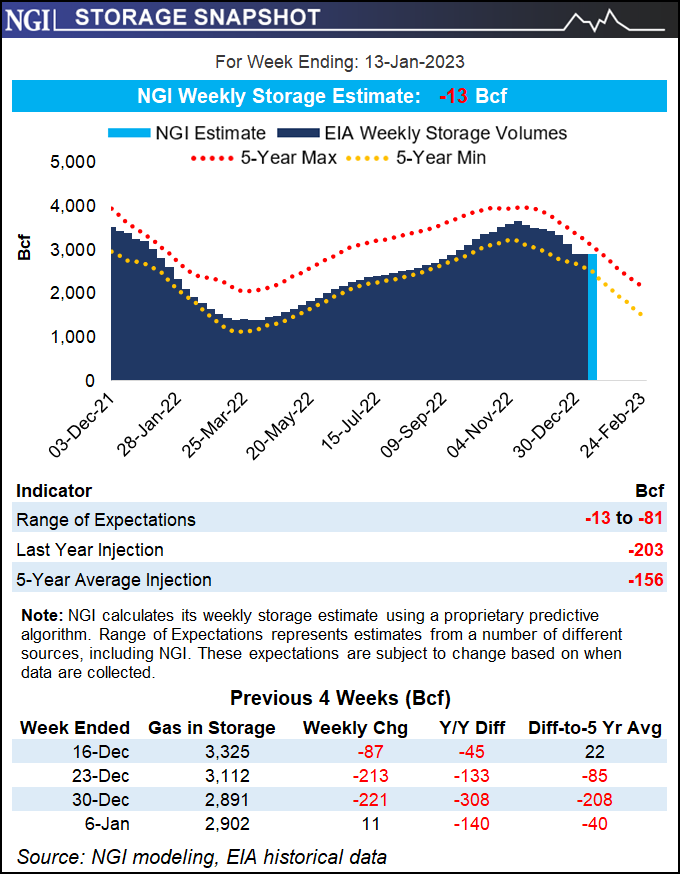

Given a selected weak climate begin to the 12 months – the primary half in January might show the warmest in almost 20 years, based on DTN – Saal mentioned the market is braced for an additional bearish storage print this week. It could comply with the uncommon January injection of 11 Bcf that the U.S. Power Data Administration (EIA) reported for the week ended Jan. 6.

The EIA report protecting the week ended Jan. 13 “goes to be manner under any historic common,” Saal mentioned. “It’s only a matter of how far under and the way it compares” to analysts’ expectations.

Estimates submitted to Reuters ranged from declines of 53 Bcf to 81 Bcf, with a median of 73 Bcf.

Bloomberg’s ballot discovered analysts in search of a median pull of 75 Bcf. Withdrawal estimates spanned from 61 Bcf to 85 Bcf.

A Wall Road Journal survey landed at a mean draw of 72 Bcf, with responses starting from decreases of 61 Bcf to 81 Bcf.

The estimates examine with a five-year common draw of 156 Bcf and a year-earlier pull of 203 Bcf.

The injection for the Jan. 6 interval in contrast with a five-year common pull of greater than 150 Bcf. It lifted inventories to 2,902 Bcf, leaving shares barely under the five-year common of two,942 Bcf and the year-earlier degree of three,042 Bcf.

Except for a possible shift within the climate, the opposite doable catalyst for pure gasoline futures is the anticipated return of Freeport LNG in Texas. The liquefied pure gasoline exporter mentioned it expects to relaunch later this month, following a June hearth and a number of other restart delays final 12 months tied to regulatory hurdles.

The corporate hopes to ramp as much as 2 Bcf/d of capability but this winter, although full restoration to 2.38 Bcf/d could not occur till the spring. That gasoline, destined for export, would come from present home provides and will assist align provide/demand balances, mentioned Marex North America LLC’s Steve Blair, senior account government.

Nonetheless, he informed NGI the market stays doubtful concerning the timing of Freeport’s return, regardless of the corporate’s latest assurances, leaving bulls “disillusioned” at this stage within the younger 12 months.

Nevertheless, “earlier than winter is over, hopefully, Freeport will take 2 Bcf/d off of the home market,” Blair mentioned.

Money Costs Fall

Spot gasoline costs rallied to start out the week amid rounds of winter climate within the West. However with temperatures typically snug elsewhere, modest demand and broader bearish sentiment sapped the momentum on Wednesday

Chicago Citygate declined 13.0 cents day/day to common $2.985, whereas Henry Hub misplaced 31.0 cents to $3.105 and Houston Ship Channel dipped 9.0 cents to $2.620.

Costs within the Rockies and California, whereas easing Wednesday, remained lofty relative to the remainder of the nation. Snow and freezing air impacted elements of the Rocky Mountain area, whereas chilly air lingered in California following a rash of heavy rains this month.

Demand has eased in California this week, as Wooden Mackenzie analyst Quinn Schulz famous, however costs within the state stay excessive partly due to provide constraints that left gasoline flows lighter than consumption at some hubs.

This included PG&E Citygate, the place common costs fell $2.090 Wednesday however remained elevated at $20.075.

Within the Rockies, Northwest Sumas shed 46.0 cents to $18.230

Trying forward, Nationwide Climate Service (NWS) information for the remainder of this week and early subsequent pointed to above-average temperatures throughout the South and East.

Chillier air that descended from Canada into elements of the West and northern Plains Wednesday was anticipated to unfold throughout a lot of the Midwest and Nice Lakes by subsequent week. NWS forecasts indicated these circumstances might advance to the South and East late within the month, driving extra heating demand.

[ad_2]

Source_link

{kind=link}